你或许会更想去 Notekit 看这份笔记

Ten Principles of Economics

Marginal Change: A small incremental adjustment to an existing plan of action.

Prices:

Determined by interaction of buyers and sellers

Reflect the good’s value to society

Reflect the cost of producing the goods

Invisible Handby Adam Smith:

- Prices guide self-interested households and firms to make decisions that maximize society’s economic well-being.

Gov: Enforce property rights.

Externality & Market Power -> Market Failure

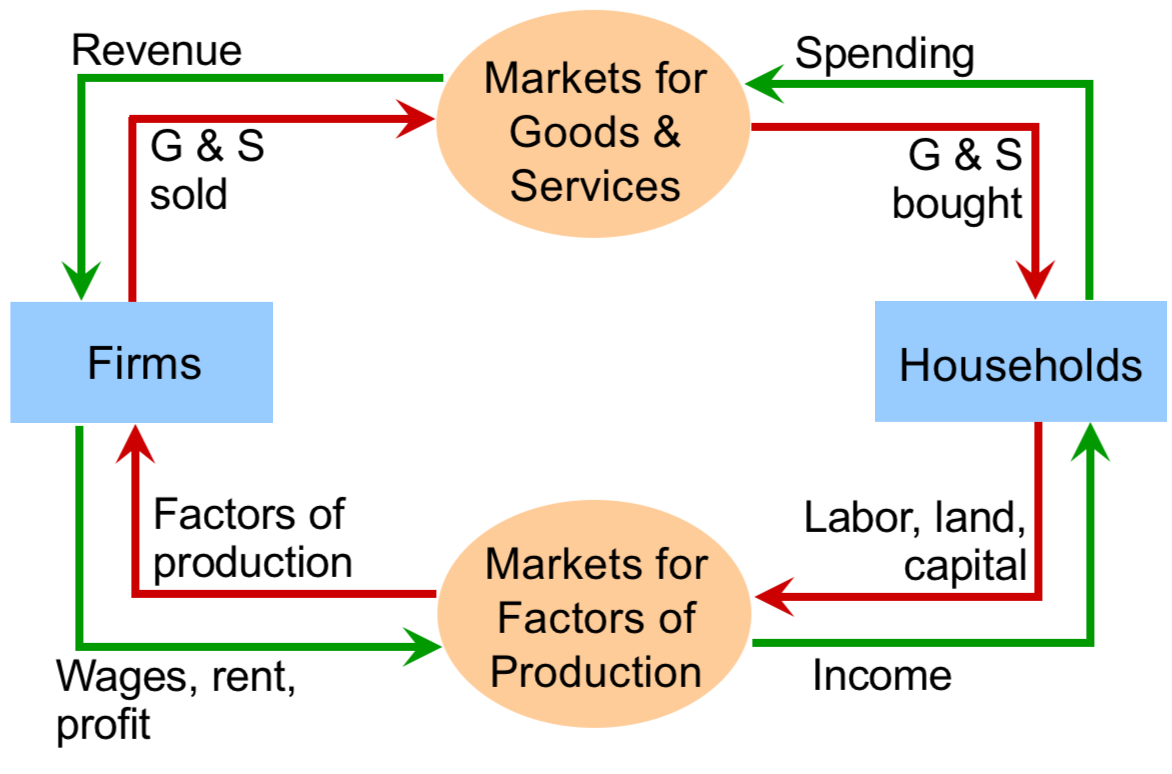

The Circular-Flow Diagram

Figure

A visual model of the economy, shows how dollars flow through markets among households and firms

Two types of “actors”

Households

Own the factors of production, sell/rent them to firms for incomeBuy and consume goods& services

Firms

Buy/hire factors of production, use them to produce goods and servicesSell goods & services

Include two markets

The market for goods and servicesThe market for “factors of production”

Positive and Normative Statement

Positive Statement: 描述现在是什么, 可以被证伪(Evaluated by analyzing data; Can be Confirmed or Refuted)

Normative Statement: 描述将来怎么样, 不可以被证伪(Evaluated using data, value judgments, views on ethics, region, political)

The Production Possibilities Frontier

PPF Example

(*现在同样的资源, 可造5000小麦或者500电脑, 电脑难造小麦容易造)

当这条线越靠近Y轴, 斜率越大时(比如X轴截距100, 说明现在的资源可造5000小麦或100电脑), 说明X轴表示的东西变得更难获得、Y轴表示的东西变得更容易获得, X轴的Opportunity Cost变大, Y轴的Opportunity Cost变小

当这条线越靠近X轴, 斜率越小时(比如X轴截距600, 说明现在的资源可造5000小麦或600电脑), 说明X轴表示的东西变得容易获得、Y轴表示的东西变得更难获得, X轴的Opportunity Cost变小, Y轴的Opportunity Cost变大

总结

靠近哪个轴这哪个轴东西容易获得, Oppurtunity Cost小 例斜率代表的是X轴所代表物品的Opportunity Cost

PPF becomes steeper and the opportunity cost of mountain bikes increases

表述:The opportunity cost of A in terms of B

Outward是凸的, Inward是凹的, Feasible是可以达到的

Usually bentoutward: due to the law of increasing opportunity cost

Resources suited to computer production are used in the car industry.

Technological advance in producing one thing: Move one endpoint while another stays the same.

Points under PPF: Not efficient(widespread unemployment); Points above PPF: Not feasible.

Comparative Advantage (-> Specialization)

Abs advantage: Produce with fewer inputs (can have in both goods)

Have lower opportunity cost than another producer (impossible to have in both goods)$$Opportunity\ Cost\ of\ A=\frac{1}{Opportunity\ Cost\ of\ B}$$

The Price of the Trade: Must lie between their opportunity costs.

Comparative Advantage -> Exports; Else Imports

International trade can make some individuals worse off, even as it makes the country as a whole better off; Same comparative advantage -> No gains

Demand & Supply

Demand:

Price Up; Quantity Down

Shift:

Increase -> Right; Decrease -> Left

Shifters:

Income

Normal Goods:((An increase in income leads to an increase in demand))

Inferior Goods:((An increase in income leads to a decrease in demand))

Prices of Related Goods

Substitutes: A’s price Up, A’s demand Down; B’s demand Up

Complements: A’s Price Up, A’s demand Down; B’s demand Down

Tastes

Expectations

Expect income Up; Current demand Up

Expect price Up; Current demand Up

Number of Buyers

Price of the good itself -> a movement along the demand curve

Supply:

Price Up; Quantity Up

Shift:

Increase -> Right; Decrease -> Left

Shifters:

Input Prices: Input price Up; The supply Down

Technology: Advance in Technology, Cost Down; Supply Up

Expectations: Expect Price Up in the future, Supply Down Today (put some of its current production into storage)

Number of Sellers

Price of the good itself represents a movement along the curve

Equilibrium Price (Marketing-clearing Price)

Surplus:$$Q_S > Q_D$$Price Down

Shortage:$$Q_D>Q_S$$Price Up

Elasticity

Price Elasticity of Demand

How much the$$Q^d$$responds to a change in price

If we say it is free to enter/leave the market, elasticity ishigh.

Determinants

Avaiability of Close Substitutes: With close substitutes -> High Elasticity

Necessities -> Inelastic; Luxuries -> Elastic

Definition Narrow -> Elastic; Broad -> Inelastic

Longer time horizons -> Elastic

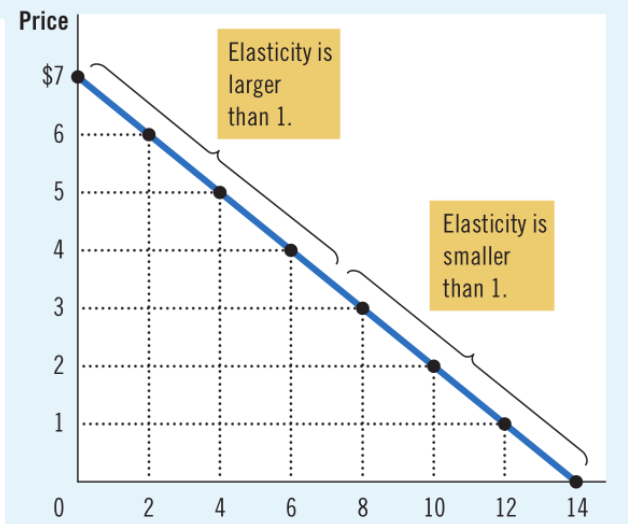

$$Price\ Elasticity\ of\ Demand = \frac{ \%\ change\ in\ Q_D}{\%\ change\ in\ Price}=\frac{\frac{Q_2-Q_1}{\frac{1}{2}(Q_2+Q_1)}}{\frac{P_2-P_1}{\frac{1}{2}(P_2+P_1)}} = \frac{(Q_2-Q_1)(P_2+P_1)}{(Q_2+Q_1)(P_2-P_1)}=\frac{P}{Q} \times \frac{1}{\frac{\Delta P}{\Delta Q} } = \frac{P}{Q} \times \frac{1}{k}$$

Whenkis a constant, (P up Q down) -> Elasticity Up.

AlwaysPOSITIVE

Variety: Elastic(>1); Unit Elastic(=1); Inelastic(<1)

注:想象Inelastic的I是竖直的, 所以竖线是Perfect Inelastic, Elasticity为0. 故斜率越大越Inelastic, 斜率越小越Elastic, 为0是横线Perfect Elastic, Elasticity为无穷

Total Revenue and the Price Elasticity of Demand

- Inelastic: Price Up, Revenue Up; Elastic: Price Up, Revenue Down; Unit Elastic: Price Change, Total Revenue Remains Constant

The Income Elasticity of Demand

$$Income\ Elasticity\ of\ Demand = \frac{ \%\ change\ in\ Q_D}{\%\ change\ in\ Income}$$

Normal Goods: Positive

Necessities: Small

Luxuries: Large

Inferior Goods: Negative

The Cross-Price Elasticity of Demand

$$CrossPrice\ Elasticity\ of\ Demand = \frac{\%\ change\ Q_D\ of\ A}{\%\ change\ P\ of\ B}$$

Substitutes: Positive; Complements: Negative

The Price Elasticity of Supply

Determinants: The flexibility of sellers to change the amount of the good they produce (Easy to change, Elasticity Up)

More elastic in the long run than short

$$Price\ Elasticity\ of\ Supply=\frac{\%\ change\ in\ Q_S}{\%\ change\ in\ P}$$

Consumer and Producer Surplus

Consumer Surplus

$$CS=WTP-P\ (*Always\ \ge 0)$$

The area below D-curve and above the Price.

Lower Price -> Additional consumer surplus to initial consumers + Consumer surplus to new consumers

Producer Surplus

$$PS=P-Cost$$

- Cost: The value of everything a seller must give up to produce a good. *Lowest price / Producer’s willingess to sell his services

The area below the Price and above the S-curve.

Higher Price -> Additional producer surplus to initial producers + Producer surplus to new producers

Market Efficiency

$$Total\ Surplus=Consumer\ Surplus+Producer\ Surplus=Value\ to\ Buyers-Cost\ to\ Sellers$$

Efficiency -> Maximize Total Surplus received by all members

Equality -> Distributing Economic Prosperity Uniformly Among the members of Society

Government Intervention

Price ceiling / Price floor

Binding 才是有效的, 即 Ceiling 高需低于 Eq’m Price 方为 Binding, Floor 需高于 Eq’m Price

DWL: Triangle Area

Labor Market: Price Floor means minimum wage. So minimum wage causes a labor surplus(unemployment).

Price ceiling -> Shortage. In the long run, supply and demand are more price-elastic. Shortage is larger.

-> Sellers must ration the goods among the buyers.

- Long lines; Discrimination according to sellers’ biases -> Often unfair and inefficient (goods do not go to buyers who value the goods most)

Apartment Rent, in the short run, we haveperfect inelastic supply.

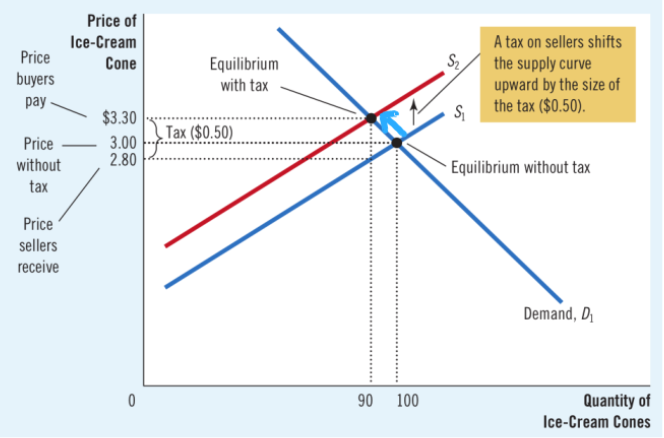

Taxes

Discourage Market Activity. Eq’m Quantity Down.

$$Tax\ Revenue=Tax \times New\ Eq’m\ Quantity$$

DWL: The fall in total surplus that results from a market distortion. Triangle Area.

Elasticity & Tax Burden

- Buyers/Sellers who havelower elasticitywill have alarger tax burden. A tax burden falls more heavily on the side of the market that is less elastic. Because fewer good alternatives and less willing to leave the market.

Thegreatertheelasticitiesof supply and demand, thelargerthedeadweight losscaused by the tax.

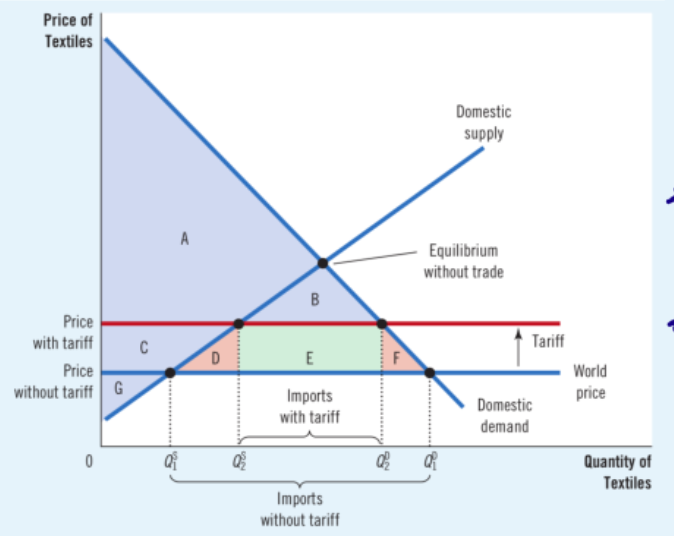

The Determinants of Trade

Word Price > Domestic Price -> Export (Opp cost low)

Word Price < Domestic Price -> Import (Opp cost high)For Exporting Country:

Domestic producers better off

Domestic consumers worse off

Economic well-being UpFor Importing Country:

Domestic consumers better off

Domestic producers worse off

Economic well-being UpTariff (Works forimporter)

a tax on imported goods

Causes DWL(Overproduction & Underconsumption). Best policy for eficiency is to allow trade without a tariff.

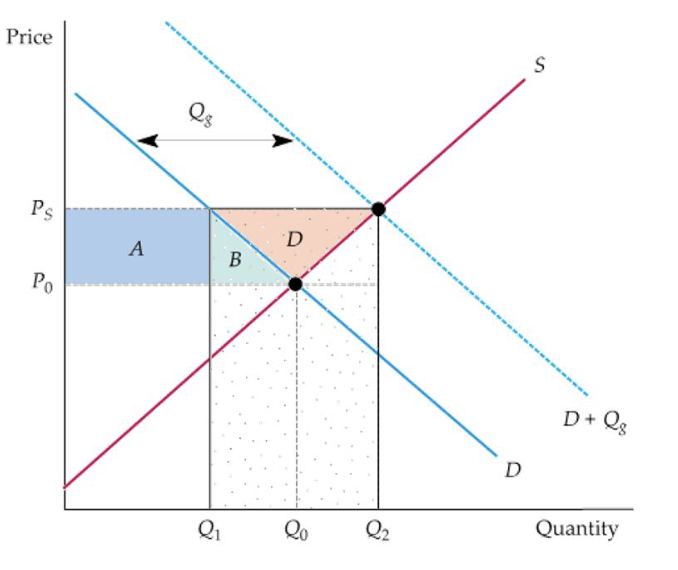

Price Support

Price Supports

$$\Delta Welfare=D-(Q_2-Q_1)\times P_S$$

$$\Delta PS = A+B+D$$

$$\Delta CS=-A-B$$

$$Gov\ Buy=Q_2-Q_1$$

$$Gov\ Cost= (Q_2-Q_1)\times P_S $$

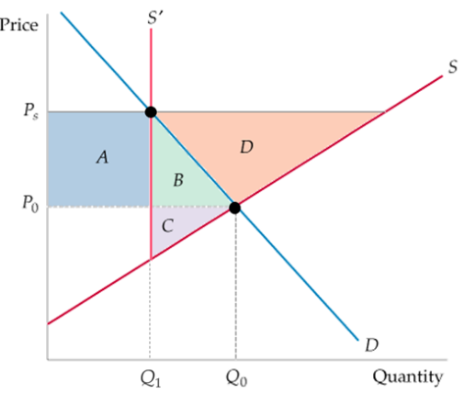

Production Quotas

$$\Delta Welfare=-(B+C)$$

Incentive Program

$$Min\ Incentive=B+C+D\ \Delta CS=-(A+B)\ \Delta PS=(A+B+D)\ \Delta Welfare=-(B+C)$$

Externality

Gov correct byinternalize the externality

Negative Externalities:$$Q^* < Q_{Market}$$, Tax

Positive Externalities:$$Q^* > Q_{Market}$$, Subsidize

Public Policies towards Externalities

Command-and-Control Policies: Regulation (Req/Forbid)

Market-based Policy: Corrective Taxes (Pigouvian Taxes) & Subsidies

$$Ideal\ Corrective\ Tax/Subsidy = External\ Cost/Benefit$$

Rather than causing DWL, actually makes the economy work better

Tradable Pollution Permits

Corrective Tax: Sets the price of pollution; Pollution: Perfectly elastic

Pollution Permits: Sets the quantity of pollution; Pollution: Perfectly inelastic

Private Solutions to Externalities

Moral Codes & Social Sanctions

Charities

Merge/ContractThe Coase Theorem

Bargain without cost over the allocation of resources -> Solve the problem of externalities on their own

Do NOT Work when

Transaction Costs are high.

A beneficial aggrement exists. Each party may hold out for a better deal.

The number of interested parties is large -> reaching efficient is difficult.

Public Goods and Common Resources

Excludability: 一个人是否可以被阻止使用

Rivalry in consumption: 一个人用是否使他人使用减少

四种分类(Congested: Rival; Toll: Excludable)

- Rival

- Not Rival

- Excludable

- Private Goods

- Congested Toll Roads

- Club Goods

- Uncongested Toll Roads

- Not Excludable

- Common Resources

- Congested Nontoll Roads

- Public Goods

- Uncongested Nontoll Roads

- ((Public Goods))underprovided

- The Free-Rider Problem

- e.g. National Defense; Basic Research(General Knowledge)

- Cost-benefit analyses are imprecise (Fair cost-sharing & Truthful Reporting)

- ((Common Resources))overconsumed

- The Tragedy of the Commons: People neglect the external cost -> overuse

- e.g. Clean Air and Water; Fish, Whales and Other Wildlife

- Regulate; Corrective Tax; Permits; Convert to private

Consumer Theory

The Budget Constraint

Limit on the consumption (bundles/combination) a consumer can afford

Slope:$$Relative\ Price=\frac{P_x}{P_y}$$

$$P_x\ x + P_y \ y=I$$

Indifference Curves

Bundles giving the consumer the same level of satisfaction.

Slope:$$MRS=\frac{MU_x}{MU_y}$$(Marginal Rate of Substitution)

他想要用几个Y轴商品换一个X轴商品, 越大说明不想要Y想要X, 越小说明不想要X想要Y.

Example: 在此点由于斜率是大的, 说明MRS是大的. 此时我有少少的x, $$MU_x$$大, 多多的y, $$MU_y$$小. 此时$$MRS=\frac{MU_x}{MU_y}$$是大的.

Assumptions:

Completeness: Consumers can compare and rank all possible baskets

Transitivity: Preferences are transitive.

More is better than less: Higher indifference curves are preferred to lower ones.

-> Properties

Higher is better.

Slope downward.

Do not cross.

Bowed inward.

Types:

Perfect Substitutes: MRS fixed, Straight lines

Close substitutes: not very bowed

Perfect Complements: MRS 0/Inf, L-shaped, right-angle

Close complements: very bowed

Utility

Score of satisfaction

Utility Function: a set of indiference curves each with anumerical indicator$$U(x,y)=2x+y \Rightarrow MU_x=2,\ MU_y=1$$

Marginal Utility(MU): Additioinal satisfaction from 1 additional unit of a good

- Diminishing Marginal Utility: More consumed, less additions to utility from additional amounts

At the optimum:$$\frac{MU_x}{P_x} =\frac{MU_y}{P_y}$$

If$$\frac{MU_x}{P_x} \gt \frac{MU_y}{P_y}$$, that means the marginal utility from an additional unit of x is larger than that of y, so we spend more on x. As we haveDiminishing Marginal Utility,$$\frac{MU_x}{P_x} \downarrow$$, finally they equal and we are at the optimum.

So$$MRS=\frac{MU_x}{MU_y}=Relative\ Price=\frac{P_x}{P_y}$$

Production Theory

Factors

Production Technology

Cost Constraints

Input Choices

Prod Func: highest output that a firm can produce for every specified combination of inputs$$q=f(K,L)$$

Production with Labor Variable

$$Marginal\ Product \gt Average\ Product \Rightarrow AP \uparrow\ MP=AP \Rightarrow AP_{max}\MP=0 \Rightarrow TP_{max}$$

Law of Diminishing Marginal Returns

- Assume that all labor inputs are of equal quality

Production with Two Variable Inputs

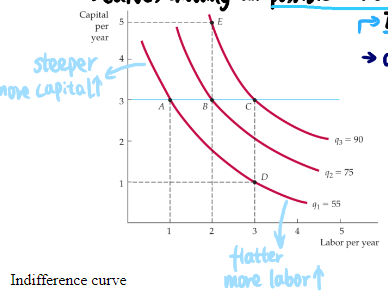

Isoquants

All possible combinations of inputs to yield the same output. 我们总是把x轴为劳动力, y轴为资本

$$A \rightarrow B \rightarrow C \Rightarrow Diminishing\ Marginal\ Returns\ to\ Labor$$第一次增加1劳动力多生产20, 第二次增加1劳动力只多生产15

$$D \rightarrow B \rightarrow E \Rightarrow Diminishing\ Marginal\ Returns\ to\ Capital$$第一次多增加1资本多生产20, 第二次15

Slope: Marginal Rate of Technical Substitution$$MRTS=\frac{MP_L}{MP_K}=-\frac{\Delta K}{\Delta L}$$

- 几个Capital能顶得上1个Labor

Downward sloping and convex

Special Cases

Perfect Substitutes: Straight Lines; MRTS Constant

Fixed-proportions Production Function: L-shaped; One labor - One capital

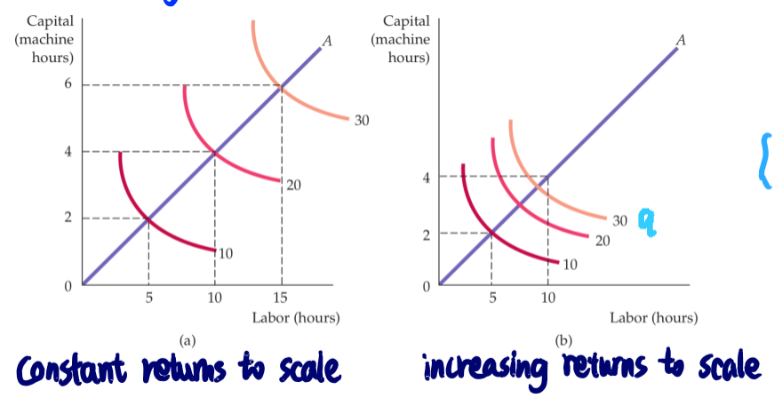

Returns to Scale

Isocosts

Cost

- $$TC=Explicit+Implicit\ Cost=FC+VC\Econ\ Profit=TR-TC\Acct\ Profit=TR-Explicit\ Cost$$

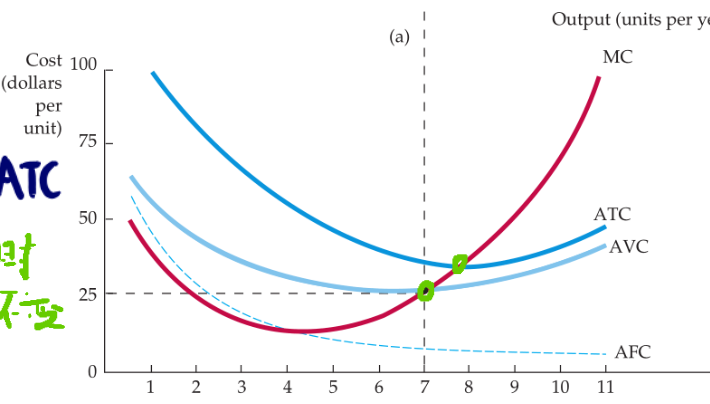

Marginal Cost:$$\uparrow Total\ Cost\ from\ 1\ extra\ unit\ Prod\MC=\frac{\Delta TC}{\Delta Q}$$

Marginal Cost corsses AVC and ATC at their minimum points.

Sunk Cost: Expenditure that has been made and cannot be recovered. 不同于Fixed Cost, 不参与重大决策

Cost in the

Short Run: Some inputs are fixed.

The determinants of Short-Run Cost

$$MC=\frac{\Delta VC}{\Delta Q}=\frac{w\Delta L}{\Delta Q}=\frac{w}{\frac{\Delta Q}{\Delta L}}=\frac{w}{MP_L}$$So$$MP_L \uparrow\ \Rightarrow MC \downarrow $$

$$Quantity\ of\ Labor \uparrow\ \Rightarrow MP_L \downarrow\ \Rightarrow\ MC\uparrow$$

Long Run: All inputs are variable.

$$User\ Cost\ of\ Capital=Economic\ Depreciation + (Interest\ Rate)\times(Value\ of\ Capital)$$

Rate(Per dollar of capital) = Depreciation rate + Interest Rate

Under competitive capital market: Rent rate = User cost = Price *Rate

Isocost Line

$$C=wL+rK\K=\frac{C}{r}-\frac{w}{r}L$$

Optimum:$$MRTS=-\frac{\Delta K}{\Delta L}=\frac{MP_L}{MP_K}=\frac{w}{r}$$

If$$\frac{MP_L}{w} \gt \frac{MP_K}{r}$$, the firm will increase the use of labor and decrease the use of capital.$$Quantity\ of\ Labor \uparrow\ \Rightarrow MP_L \downarrow$$Finally we get to the optimum.

Competitive Market

Assumption: Perfectly Competitive Market

Market with many buyers and sellers.

All the products are identical.

Firms can freely enter or exit the market.

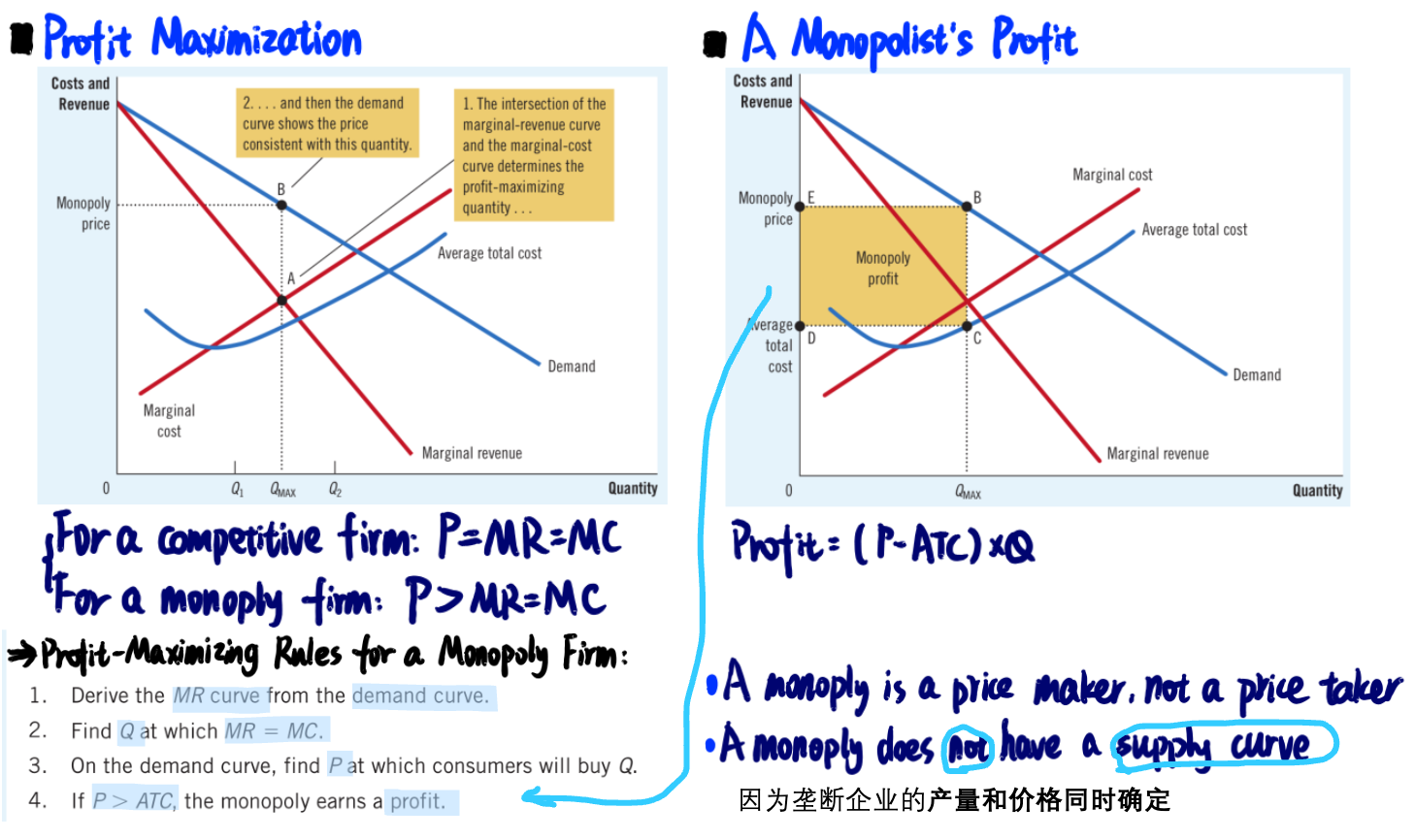

-> For competitive firms,$$AR=MR=P$$

$$TR=PQ\AR=\frac{TR}{Q}\MR=\frac{\Delta TR}{\Delta Q}\Profit_{max}\ when\ MR=MC$$

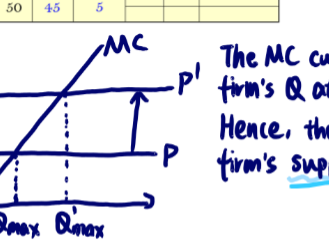

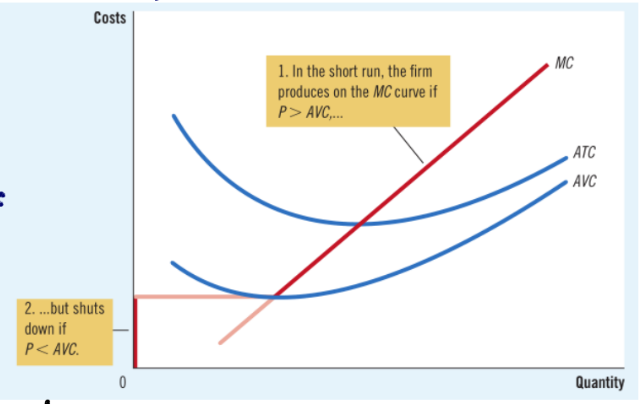

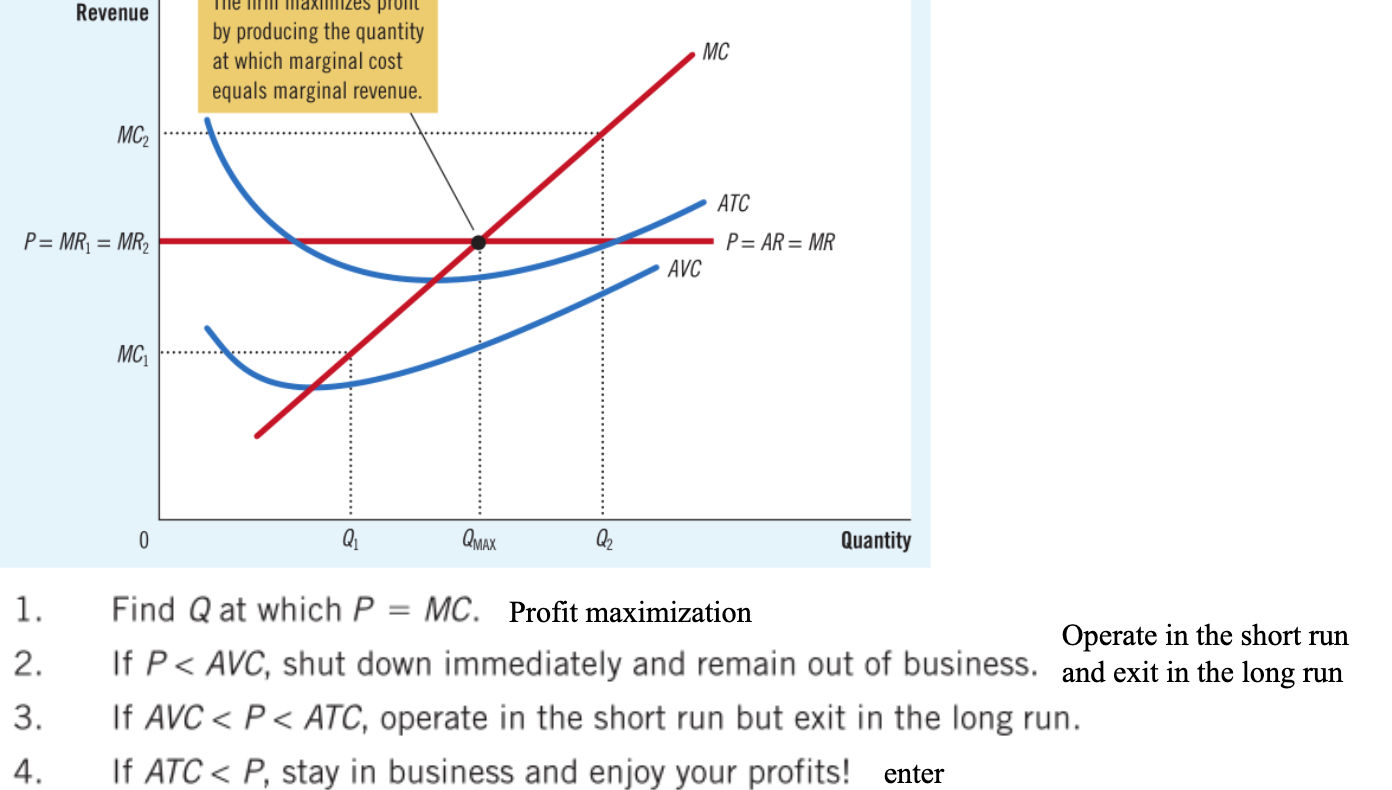

MC determines Q at any price. The competitive firm’sShort-Run Supply Curveis the portion of itsMC Curvethat lies above theAVC Curve.

The firm choose to shut down if$$TR<VC\ \ P<AVC$$

The firm choose to shut down if$$TR<VC\ \ P<AVC$$After shutting down, still need to pay fixed cost.

In the short run, FC are sunk costs, thus FC should not matter in the short-run decision.

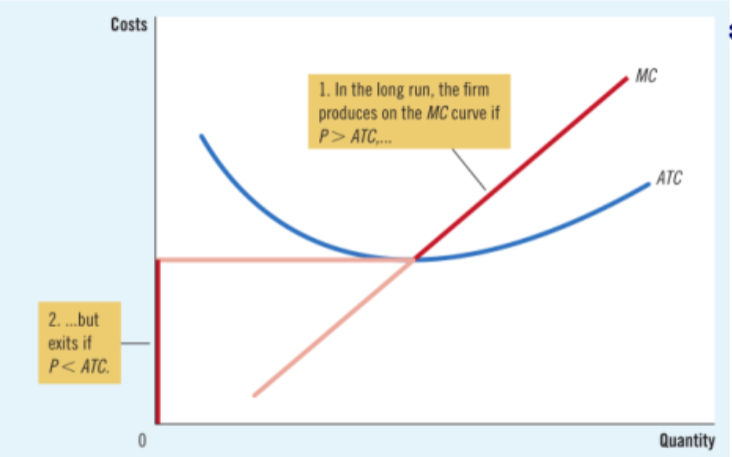

The competitive firm’sLong-Run Supply Curveis the portion of itsMC Curvethat lies above theATC Curve.

Long-Run Decision to Exit or Enter a Market

The firm choose to exit if$$TR<TC\ \ P<ATC$$to enter if$$TR>TC\ \ P>ATC$$

- After exit, 0 cost.

$$Profit=TR-TC=(P-ATC)\times Q$$

Firm

The Supply Curve in a Competitive Market

The Short-Run: With a Fixed Number of Firms (Usually upward-sloping line)

The Long-Run: Market Supply with Entry and Exit

因为有profit时就会有enter, supply增加price降低profit下降

有loss时就会有exit, supply减少price升高profit增加$$Price=Marginal\ Cost=Average\ Total\ Cost$$

At the minimum of ATC

Why Zero Profit?

- Profit includes all includes all implicit costs. So when econ profit is zero, acct profit is positive.

Why Long-Run Supply Curve Might Slope Upward?

Horizontal: All firms have identical costs, and costs do not change as other firms enter or exit the market.

Upward: Firms have diferent costs, or cost rise as firms enter the market.

- The price in the market reflects the average total cost of the marginal firm.

Monopoly

Types

Monopoly Resources

Government Regulation

Natural Monopolies

Increasing Q ->

Higher output raises revenue

Lower price reduces revenue

To sell a larger Q, the monopolist must reduce the price on all the units it sells. => Marginal revenue is less than the price of its good.

MR can be negative. Price effect on revenue outweighs the output effect.

$$Profit\ Maximization\ P>MR=MC\ For\ a\ competitive\ firm:\ P=MR=MC$$

在”Monopoly quantity” 右侧的某一单位产量, 消费者愿意支付的价格高于企业生产该单位的成本, 但这一单位产量没有被生产出来, 这就造成了社会福利的损失, 累积起来就是图中的红色阴影部分.

Price Regulation

The Effect of Tax

$$MR=\frac{\Delta R}{\Delta Q}=\frac{\Delta (PQ)}{\Delta Q}=P+Q \frac{\Delta P}{\Delta Q}=P+P(\frac{Q}{P})(\frac{\Delta P}{\Delta Q})=P+P(\frac{1}{E_d})=MC$$

$$P=\frac{MC}{1+\frac{1}{E_d}}$$

$$Markup=Lerner\ Index=\frac{P-MC}{P}=-\frac{1}{E_d}$$